Published: 10 March 2026

The 18th edition of W Hospitality Group's annual survey has a record 53 international and regional (African) contributors, reporting pipeline activity in Africa totalling 123,846 rooms in 675 hotels and resorts, up 18.6 per cent on 2025. The total includes four new contributors this year with 6,636 pipeline rooms between them – on a same-store basis, the increase is still a very commendable 12.2 per cent, much higher than what the international majors report for global pipeline growth. More detail will be available in the main report.

These are the five-year total pipeline figures:

| Hotel Chain Development Pipelines in Africa 2026 Regional Summary |

||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| 2022 | 2023 | 2024 | 2025 | 2026 | ||||||

| Hotels | Rooms | Hotels | Rooms | Hotels | Rooms | Hotels | Rooms | Hotels | Rooms | |

| North Africa | 166 | 35,280 | 175 | 36,677 | 192 | 40,134 | 230 | 49,260 | 284 | 62,630 |

| Sub-Saharan Africa | 281 | 45,011 | 307 | 47,750 | 332 | 52,059 | 347 | 55,184 | 391 | 61,216 |

| TOTAL | 447 | 80,291 | 482 | 84,427 | 524 | 92,193 | 577 | 104,444 | 675 | 123,846 |

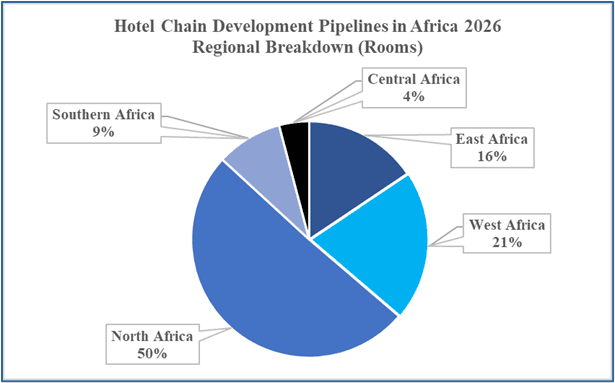

The regions are very different, with just four countries represented in North Africa (Morocco, Algeria, Tunisia and Egypt) and 38 in sub-Saharan Africa; that’s 42 countries (out of 54) with a pipeline, leaving 12 without any recorded deals (the same as last year). Simplistically that’s about 70 potential new hotels per country in North Africa, and just 10 per country in sub-Saharan Africa. The countries with the largest pipelines in North Africa are Egypt and Morocco, and in sub-Saharan Africa it’s Cape Verde, Ethiopia, Kenya and Nigeria, unchanged from last year.

Morocco and Egypt together comprise over 45 per cent of the total pipeline rooms, and that share is growing, because that is where the chains are signing the most deals. In 2025, the chains report signing about 60 deals in the two countries, which is 40 per cent of the 150 continent-wide signings; the next largest number was 17 signed deals in Kenya. For the other regions.

When analysed according by the number of rooms in their pipeline, the top ten countries account for 75 per cent of the total hotels in the survey, and 79 per cent of the rooms, both figures a few percentage points up on last year – they also account for over 75 per cent of last year’s signings, signalling even greater dominance in the future.

| Hotel Chain Development Pipelines in Africa 2026 Top 10 Countries by Number of Rooms |

||||

|---|---|---|---|---|

| Hotels | Rooms | Average Size | ||

| 1 | Egypt | 185 | 45,984 | 249 |

| 2 | Morocco | 75 | 10,606 | 141 |

| 3 | Nigeria | 57 | 8,480 | 149 |

| 4 | Kenya | 35 | 6,190 | 177 |

| 5 | Ethiopia | 34 | 5,964 | 175 |

| 6 | Cape Verde | 17 | 4,328 | 255 |

| 7 | Tunisia | 15 | 4,189 | 279 |

| 8 | Tanzania | 29 | 4,159 | 143 |

| 9 | South Africa | 31 | 4,136 | 133 |

| 10 | Ghana | 26 | 3,942 | 152 |

Year after year Egypt leads the country table, now with almost 46,000 rooms in 185 hotels, there were 39 new deals signed last year, and is an apparently unassailable position, with over four times the number of rooms in second-placed Morocco and over one third of the entire pipeline rooms. The pipeline in Egypt is increasing substantially and the number of hotels and resorts actually in operation is showing slow growth, with seven openings last year compared to just three in 2024. This is due, we believe to the relatively young pipeline, with 60 per cent of the projects there (111 deals) signed in 2022 and later, and therefore perhaps too “young” to be actualised. The chains anticipate opening 33 properties in Egypt in 2026.

| Hotel Chain Development Pipelines in Africa 2026 Top 10 Countries by Pipeline Status |

|||||

|---|---|---|---|---|---|

| Hotels | Rooms | ||||

| Total | Onsite Construction | ||||

| 1 | Egypt | 185 | 45,984 | 23,622 | 51.4% |

| 2 | Morocco | 75 | 10,606 | 6,859 | 64.7% |

| 3 | Nigeria | 57 | 8,480 | 3,328 | 39.2% |

| 4 | Kenya | 35 | 6,190 | 4,922 | 79.5% |

| 5 | Ethiopia | 34 | 5,964 | 4,768 | 79.9% |

| 6 | Cape Verde | 17 | 4,328 | 374 | 8.6% |

| 7 | Tunisia | 15 | 4,189 | 2,673 | 63.8% |

| 8 | Tanzania | 29 | 4,159 | 3,222 | 77.5% |

| 9 | South Africa | 31 | 4,136 | 2,778 | 67.2% |

| 10 | Ghana | 26 | 3,942 | 2,196 | 55.7% |

Egypt has just over 50 per cent of rooms onsite - compare that to Morocco, with over 72 per cent. Of the top 10 countries, Ethiopia and Kenya have the highest ratio of rooms under construction, followed by Tanzania and South Africa. Cape Verde stands out as having a very low percentage of projects under construction, reflective of increased planning activity as well as new contributors who focus majorly or entirely on that country. Note of course that that “under construction” does not necessarily mean that there is activity and progress towards opening – many of the sites in Nigeria and Ghana, for example, have been closed for several years, with some pretty impressive trees growing out of the roofs and balconies!

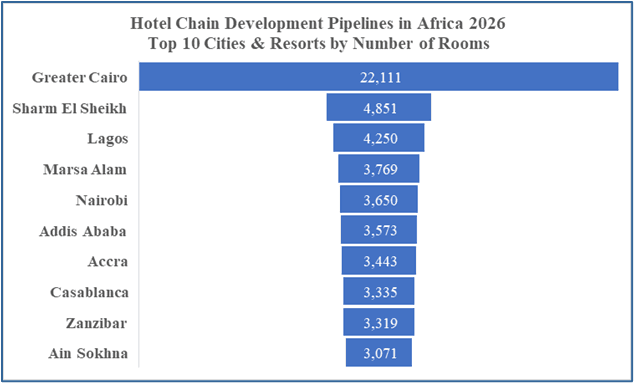

Greater Cairo again has by far the largest pipeline (18 per cent of the entire pipeline, a little up from 17 per cent last year), followed by Sharm El Sheikh and Lagos.

The flurry of signings in Egypt last year results in two resorts, Marsa Alam and Ain Sokhna, joining the top ten. In percentage terms, the number of rooms in resort projects is increasing much faster than those in city hotels, driven by the number of signings and also by the larger average size of the resorts (205 keys vs. 174). Added to that, just under half of the rooms in properties that opened last year were in resorts.

The Big 5 global chains – Marriott International, Hilton, Accor, Radisson Hotel Group and IHG Hotels & Resorts – account for about 80 per cent both of hotels and of rooms in the entire African pipeline:

| Hotel Chain Development Pipelines in Africa 2026 Top 10 Hotel Chains by Number of Planned Hotels and Resorts |

||||||

|---|---|---|---|---|---|---|

| Hotel Chain | Hotels | Rooms | Change on 2025 | Average Size | Share of Total | |

| 1 | Marriott International | 180 | 31,782 | 7% | 177 | 25.7% |

| 2 | Hilton | 109 | 19,599 | 15% | 180 | 15.8% |

| 3 | Accor | 88 | 18,298 | 22% | 208 | 14.8% |

| 4 | IHG Hotels & Resorts | 48 | 9,495 | 19% | 198 | 7.7% |

| 5 | Radisson Hotel Group | 35 | 7,220 | 14% | 206 | 5.8% |

| 6 | Kerten Hospitality | 17 | 3,185 | 69% | 187 | 2.6% |

| 7 | Jaz Hotel Group | 13 | 2,651 | - | 204 | 2.1% |

| 8 | CityBlue Hotels | 12 | 2,650 | 183% | 221 | 2.1% |

| 9 | The Ascott | 20 | 2,419 | 28% | 121 | 2.0% |

| 10 | Rotana | 10 | 2,282 | - | 228 | 1.8% |

Marriott International continues to have by far the largest pipeline, in keeping with its global position (c610,000 pipeline rooms and an existing system of 1.8 million). They have over 60 per cent more rooms than second-placed Hilton (with a global total of c520,000 pipeline rooms and a system of 1.3 million rooms), but note that other chains are recording greater pipeline growth percentages (albeit all on much lower bases). It is encouraging to see that the international chains are, by and large, reporting much higher percentage growth in their African pipelines than their global pipeline growth, averaging around 4 to 6 per cent.

Looking at the 168 brands with which the chains are seeking to increase their system footprint in Africa, Hilton (the brand) leads, and the eponymous chain also counts its Hilton Garden Inn and DoubleTree by Hilton brands in the top 5, with a total of 16,235 between the three of them. Marriott tops that with four brands, but second with a total of 15,181 rooms in the top ten. However, Marriott International (the chain) has no fewer than 26 brands with signed deals in Africa, compared to 11 for Hilton, which must be one of the reasons for its dominance of the chains’ rankings. The top ten brands account for 32 per cent of the total.

| Hotel Chain Development Pipelines in Africa 2026 Top 10 Brands by Number of Planned Hotels and Resorts |

||||||

|---|---|---|---|---|---|---|

| Brand | Hotels | Rooms | Change on 2025 | Average Size | Share of Total | |

| 1 | Hilton | 35 | 8,550 | 12.9% | 244 | 6.9% |

| 2 | Marriott Hotels & Resorts | 23 | 6,339 | 17.8% | 276 | 5.1% |

| 3 | Hilton Garden Inn | 26 | 4,033 | 29.4% | 155 | 3.3% |

| 4 | DoubleTree by Hilton | 21 | 3,652 | -6.1% | 174 | 2.9% |

| 5 | Protea Hotels | 24 | 3,422 | 6.4% | 143 | 2.8% |

| 6 | Rixos | 5 | 3,295 | 33.6% | 659 | 2.7% |

| 7 | Four Points by Sheraton | 19 | 3,224 | -12.0% | 170 | 2.6% |

| 8 | Radisson | 15 | 2,693 | 21.7% | 180 | 2.2% |

| 9 | Radisson Blu | 9 | 2,216 | 11.5% | 246 | 1.8% |

| 10 | Courtyard by Marriott | 10 | 2,196 | 5.8% | 220 | 1.8% |

Of the total 123,846 rooms in the pipeline, over 65,000 rooms (almost 53 per cent) are expected by the hotel chains to open in 2026 and 2027. However, a rather concerning 20 per cent of those openings are reported to be still not yet under construction – maybe the owners didn’t tell the chains that they’re already doing the final fix! The actualisation rate (actual openings vs. expected openings) in 2025 was about one third, so on that basis what we might see this year is around 11,000 new rooms – of course we hope for more!

| Hotel Chain Development Pipelines in Africa 2026 Anticipated Opening Years of Pipeline Deals |

|||

|---|---|---|---|

| Anticipated Opening Date | Hotels | Rooms | Cumulative New Rooms Open |

| 2026 | 183 | 31,768 | 31,768 |

| 2027 | 177 | 33,381 | 65,149 |

| 2028 | 131 | 25,065 | 90,214 |

| 2029 | 60 | 11,001 | 101,215 |

| To Be Confirmed | 124 | 22,631 | 123,846 |

Historical data suggest that the expectations of opening years tend to be optimistic, but that’s not a bad thing, it’s a reflection of the optimism generally – from owners and operators alike, for the future growth of Africa’s hotel industry.

Note:

These are the highlights from the full report, which can be downloaded shortly after FHS Africa from www.w-hospitalitygroup.com. Trevor Ward will be presenting details from the report at the event.

About W Hospitality Group:

The W Hospitality Group, a founder member of Hotel Partners Africa, specialises in the provision of advisory services to the hotel, tourism and leisure industries in Africa. With experience of 40 countries on the continent, the firm is generally acknowledged as the most authoritative source on the hotel sector’s growth and performance.

info@W-HospitalityGroup.com